Insurance — Protect What Matters Most

Clear guidance on the cover you need, why it’s important, and how to find the right protection at a competitive price.

Understanding Insurance Cover

Life Insurance

Life insurance is often considered a key component of a protection strategy. In the event of death, it can provide a lump sum payment to beneficiaries, which may be used for a range of financial needs such as repaying a mortgage, assisting with education costs, replacing lost income, or covering funeral expenses.

The level of cover required will vary depending on factors such as outstanding debts, dependants, income, and the period your family may need financial support. Policies may be held either inside or outside superannuation, with different ownership structures and potential tax considerations.

Total & Permanent Disability (TPD)

Own Occupation — You may be considered totally and permanently disabled if illness or injury prevents you from ever working in your specific occupation again. This definition generally provides broader coverage.

Any Occupation — You may be considered totally and permanently disabled only if you are unable to work in any occupation reasonably suited to your education, training, or experience. This definition is more restrictive and is typically the option available when held inside superannuation.

TPD cover is often arranged alongside life insurance. The level of cover required may be similar to life insurance needs, with additional consideration for rehabilitation, medical expenses, and potential long-term financial support.

The appropriate definition and level of cover will depend on your individual circumstances.

Income Protection

Waiting period: The time between when you stop working due to illness or injury and when benefit payments begin (commonly 30, 60, or 90 days). Choosing a longer waiting period may reduce premiums, and some people rely on savings or available leave to cover expenses during this time.

Benefit period: The length of time payments may continue while you remain unable to work (commonly two years, five years, or to age 65). Longer benefit periods generally increase the cost of cover but extend the duration of potential support.

Trauma / Critical Illness

Personal Protection

Protect Your Family From Debt

Children's Education & Upbringing

Replace Lost Income

Legacy & Lifestyle Continuity

How Much Cover Do You Want?

- General Information Only

How Much Cover Do You Want?

- Life Insurance Guide

$

- TPD Guide

$

- Income Protection Guide

$

This is a starting point. Your actual needs depend on your individual circumstances, existing cover, and financial goals.

- Trauma Guide

–

Business Protection — Same Products, Smarter Strategy

- Key Person Insurance

Safeguards the business if a key individual dies or becomes disabled. The policy is owned by the business, and any benefit paid goes directly to the business.

Revenue Purpose

Capital Purpose

- Buy/Sell Insurance

Ownership Structures Compared

| Structure | How It Works | Premiums | CGT on Proceeds | Best For |

|---|---|---|---|---|

| Self-Owned | Each partner holds a policy on their own life. If a claim occurs, the benefit is paid to the departing owner or their estate. | Not deductible (capital purpose) | No CGT if original owner | Simplicity, tax efficiency |

| Cross-Owned | Each partner holds a policy on the other partner’s life. If a claim occurs, the payout goes to the surviving partners. | Not deductible (capital purpose) | CGT applies on TPD & Trauma (unless spouse/relative) | Certainty of funds for survivors |

| Trust-Owned | A trust structure owns and manages the insurance policies on behalf of the partners. | Not deductible (capital purpose) | Depends on trust deed (capital vs income characterisation) | Flexibility, multiple partners |

- Warning: Without a properly structured buy–sell agreement, the departing owner or their estate may receive the insurance payout while still retaining their ownership stake in the business. The insurance only works as intended when a formal agreement is in place.

- Division 7A & FBT risks: If a company covers insurance premiums for partners without the correct structure in place, it may trigger Division 7A deemed dividend issues or Fringe Benefits Tax implications. It’s important to obtain specialist advice on how the policy is owned and how premiums are paid.

- Business Expenses Insurance

- Revenue Protection

Inside Super vs Outside Super

| Factor | Inside Super | Outside Super |

|---|---|---|

| Cost | ✅ Premiums paid from super balance (not your pocket) | ❌ Paid from after-tax income |

| Impact on Retirement | ❌ Reduces your super balance over time | ✅ No impact on super savings |

| Tax on Premiums | ✅ Effectively paid with 15% tax money | Varies — IP premiums are tax-deductible outside super |

| Tax on Payouts | ❌ May be taxed depending on age and components | ✅ Generally tax-free (life & TPD to dependants) |

| TPD Definition | ❌ Limited to "Any Occupation" definition | ✅ "Own Occupation" available |

| Trauma Cover | ❌ Cannot be held inside super | ✅ Available outside super only |

| Claims Process | ❌ Must go through super trustee — can be slower | ✅ Direct claim with insurer |

- The bottom line: Many Australians have insurance inside their super by default — and that may not be enough, or may not be the right structure. The right mix of inside and outside super depends on your income, tax position, age, and goals.

How to Choose an Insurer

Insurance policies can vary significantly. Understanding those differences can save you thousands — or make all the difference when you need to claim.

What Affects Your Premium?

- Age — Premiums increase as you get older

- Gender — Statistically different risk profiles

- Smoker status — Smokers pay significantly more

- Occupation — Higher-risk jobs mean higher premiums

- Health history — Pre-existing conditions may affect cover or cost

- Cover amount & type — More cover = higher premiums

Beyond the Price Tag

- PDS definitions matter — The cheapest policy may have the strictest definitions, making it harder to claim

- Claims support — How does the insurer handle claims? Do they have a good reputation?

- Policy features — Built-in benefits, indexation, guaranteed renewability

- Financial strength — Is the insurer well-capitalised and likely to be around when you need them?

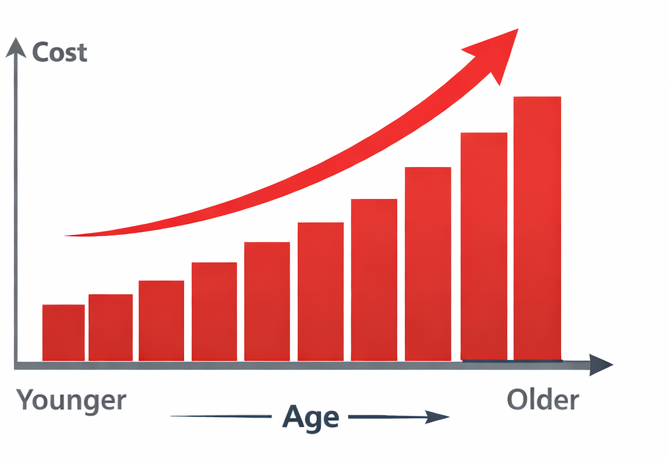

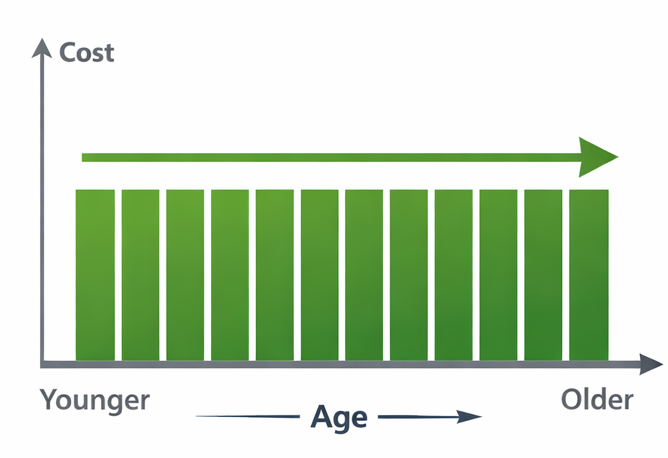

Stepped vs Level Premiums

Stepped Premiums

Level Premiums

Note: Level premiums are not truly “level” — they can still increase due to CPI and insurer rate changes. But they don’t increase purely because of your age.

Why Work With an Adviser?

Access to Multiple Insurers

Tailored Needs Analysis

Claims Advocacy

Ongoing Reviews

- We research and compare policies across the market on your behalf.